The strategic use of AP Inter 1st Year Economics Model Papers Set 4 allows students to focus on weaker areas for improvement.

AP Inter 1st Year Economics Model Paper Set 4 with Solutions

Time: 3 Hours

Maximum Marks: 100

Section – A

I. Answer any Three of the following questions in not exceeding 40 lines each. (3 × 10 = 30)

Question 1.

Explain how Robbin’s definition is superior to the welfare definition.

Answer:

Lionel Robbin’s of London School of Economics introduced the ‘Scarcity’ definition of Economics, in his book.

‘An Essay on the nature and significance of Economic Science’. According to Robbin’s “Economics is the science which studies human behaviour as a relationship between ends and scarce means which have alternative uses”. Scarcity of resources is the central idea in Robbin’s definition.

Main features of Robbin’s definition :

- Unlimited wants or ends

- Means are scarce or limited .

- Means have alternative uses

- Problem of choice.

Welfare definition:

According to Marshall “Economics is on one side a study of wealth and on the other and more important side a part of study of man.” Marshall in his definition gave more importance to man than wealth. Marshall defined “Political economy or Economics is a study of mankind in the ordinary business of life, it examines that part of individual and social action which is most closely connected with the attainment and with the use of the material requisites of wellbeing.

Main features of welfare definition:

- He assumed that Economics must be a science which is study of man kind in the ordinary business of life.

- Economics is concerned with real man influenced by hu-man considerations and it has no concern with the political, social and religious aspects of life.

- Wealth is a means for promoting human welfare.

- The main emphasis of Marshall is on material welfare and the immaterial aspects are ignored.

Superiority of Robbin’s definition over Marshall’s definition:

- According to Marshall “Economics Studies the activities of those people who live in society”. But Robbin’s says that Economics studies, all human activities whether they promote human welfare or not.

- According to Marshall “The scope of Economics is limited. But Robbin’s the scope of Economics is wide”.

- Robbin’s definition has universal applicability. Because it is applicable to all types of societies.

- Robbin’s definition of Economics is neutral between ends. He made economics a positive science. It does not pass value judgements.

![]()

Question 2.

Distinguish between internal and external economies.

Answer:

Economies of large scale production can be’ grouped into two types.

1) Internal economies

2) External economies.

1. Internal Economies:

Internal economies are those which arise from the expansion of the plant, size or from its own growth. These are enjoyed by that firm only. “Internal economies are those which are open to a single factory or a single firm independently of the action of other firms”. – Cairncross

i) Technological Economies:

The firm may be running many productive establishments. As the size of the productive establish-ments increase, some mechanical advantages may be obtained. Economies can be obtained from lihking process to another pro-cess i.e. paper making and pulp making can be combined. It also used superior techniques and increased specialization.

ii) Managerial Economies:

Managerial economies arises from specialisation of management and mechanisation of mana-gerial functions. For a large size firm it becomes possible for the management to divide itself into specialised departments under specialised personnel. This increases efficiency of management at all levels. Large firms have the opportunity to use advanced tech-niques of communication, computers etc. All these things help in saving of time and improve the efficiency of the management.

iii) Marketing Economies:

The large firm can buy raw ma-terials cheaply, because it buys in bulk. It can secure special con-cession rates from transport agencies. The product can be adver-tise better. It will be able to sell better.

iv) Financial Economies:

A large firm can arise funds more easily and cheaply than a small one. It can borrow from bankers upon better security.

v) Risk bearing Economies:

A large firm incurs unrisk and it can also reduce risks. It can spread risks in different ways. It can

undertake diversifications of output. It can buy raw materials from several firms.

vi) Labour Economies:

A big firm employs a large number of workers. Each worker is given the kind of Job he is fit for.

2. External Economies: An external Economies is one which is available to all the firms in an industry. External economies are available as an industry grows in size.

i) Economies of concentrations:

When a number of firms producing an identical product are localised in one place, certain facilities become available to all Ex: cheap transport facility, avail-ability of skilled labour etc

ii) Economies of information : When the number of firms in an industry increases collective action and co-operation effort becomes possible. Research work can be carried a jointly scientific journal can be published. There is possibility for exchange of ideas.

iii) Economies of Disintegration: When the number of firm increases the firm may agree to specialise. They may divide among themselves the type of products of stages of production Ex: cotton industry.

Question 3.

Compare the features of perfect competition and monopoly market.

Answer:

Perfect competition and monopoly are two important lands of market situations. In actual world both perfect competition and pure monopoly do not exist. The following are the similarities and differences between the perfect competition and monopoly.

Similarities :

- Both a perfect competitor and monopolist aim at maximisation of profits.

- Both monopoly and perfect competition firms attains equilibrium under the same condition, viz, MC = MR.

- The cost curves tend to be ‘U’ shaped in both the markets.

- In both markets, products are homogeneous. Differences between perfect competition and monopoly:

| Perfect competition | Monopoly |

| 1. There is large number of sellers. | 1. There is only one seller. |

| 2. All products are homogeneous. | 2. No close substitutes. |

| 3. There is freedom of free entry and exists. | 3. There is no freedom of free entry and exists. |

| 4. There is difference between industry and firm. | 4. Industry and firm both are same. |

| 5. Industry determines the price and firm receives the price. | 5. Firm alone determine the price. |

| 6. There is universal price. | 6. Price discrimination is possible. |

| 7. The AR, MR curves are parallel to ‘X’ axis. | 7. The AR, MR curves are different and slopes downs from left to right. |

Question 4.

Explain marginal productivity Theory of Distribution.

Answer:

This theory was developed by J.B.Clark. According to his theory, the remuneration of a factor of production will be equal to its marginal productivity. The theory assumes perfect competition in the market for factors of production. In such a market, average cost and marginal cost of each unit of factor of production are the same as they are equal to the price or cost of a factor of production.

For example if four tailors can stitch ten shirts in a day and five tailors can stitch thirteen shirts in a day, then the marginal physical product of the 5th tailor is 3 shirts. If stitching charge for a shirt is ₹ 100/- , then the marginal value product of three shirts is ₹ 300/-. According to this theory the 5th person will be remunerated ₹ 300/- marginal physical product is the additional output obtained by using an additional unit of the factor of production. If we multiply the additional output by market price we will get marginal value product or marginal revenue product.

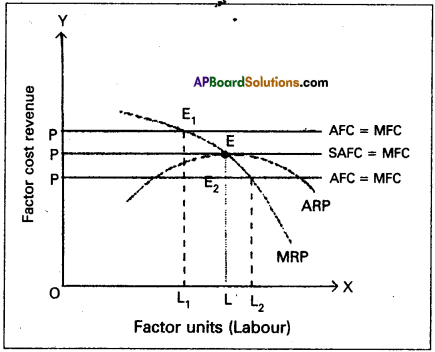

At first stage when additional units of labour are employed the marginal productivity of labourer increases up to certain extent due to economies of scale. If additional units of labour are employed beyond that point the marginal productivity of labour decreases. This can be shown in the following figure.

In the figure ‘OX’ axis represent units of labour and ‘OX’ represent price/revenue/cost. At given price ‘OP’ the firm will employ OL units of labour where price OP = L. If it employees less than ‘OL’ ie., OL, units MRP will be E1L1, which is higher than the price OR If firm employers more than ‘OL’ units up to OL2 price is OP is more than E2l2. So the firm decreases employment until price = MRP till OL. At that point ‘E’ the additional limits of labour is remunerated equal to his marginal productivity.

![]()

Question 5.

Discuss the implication of the classical theory of employment.

Answer:

The theory of output and employment developed by economists such as Adam Smith, David Ricardo, Malthus is known as classical theory. It is based on the famous “Law of markets” advocated by J.B. Say. According to this law “supply creates its own demand”. The classical theory of employment assumes that there is always full employment of labour and other resources. The classical economists ruled out any general unemployment in the long run. These views are known as the classical theory of output and employment.

The classical theory of employment can be three dimensions.

A. Goods market equilibrium

B. Money market equilibrium

C. Equilibrium of the labour market (Pigou wage cut policy)

A) Goods market equilibrium:

The 1st part of Say’s law of markets explains the goods market equilibrium. According to Say “supply creates its own demand”. Say’s law states that supply al-ways equals demand. Whenever additional output is produced in the economy, the factors of production which participate in the process of production. The total income generated is equivalent to the total value of the output produced. Such income creates addi-tional demand for the sale of the additional output. Thus there could be no deficiency in the aggregate demand in the economy for the total output. Here every thing is automatically adjusting without need of government intervention.

The classical economists believe that economy attains equi-librium in the long run at the level of full employment. Any dis-equilibrium between aggregate demand and aggregate supply equi-librium adjusted automatically. This changes in the general price level is known as price flexibility.

B) Money market equilibrium:

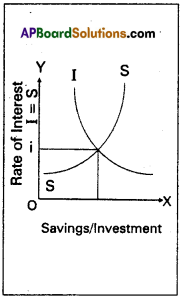

The goods market equilibrium leads to bring equilibrium of both money and labour markets. In goods market, it is assumed that total income spent the classical economists agree that part of the income may be saved. But the savings is gradually spent on capital goods. The expenditure on capital goods is tailed investment. It is assumed that equality between savings and investment is brought by the flexible rate of interest. This can be explained by the following diagram.

In the diagram savings and Investment are measured on the X’ axis and rate of interest on V axis. Savings and investments are equal at ‘Oi’ rate of interest. So money market equilibrium can be automatically brought through the rate of interest flexibility.

C) Labour market equilibrium:

According to the classical economists, unemployment may occur in the short run. This is not because the demand is not sufficient but due to increase in the wages forced by the trade unions. A.C. Pigou suggests that reduction in the wages will remove unemployment. This is called wage – cut policy. A reduction in the wage rate results in the increase in employment. .

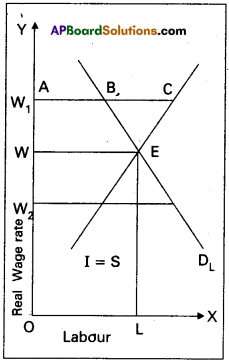

According to the classical theory supply of and demand for labour are determined by real wage rate. Demand for labour is the inverse function of the real wage rate. The supply of labour is the direct function of real wage rate. At a particular point real wage rate the supply of and the demand for labour in the economy be¬come equal and thus equilibrium attained in the labour market. Thus there is full employment of labour. This can be explained with the help of diagram.

In the above diagram supply of and demand for labour is mea¬sured on the X – axis. The real wage rate is measured on the T axis. If the wage rate is OWj, the supply of labour more than the demand for labour. Hence the wage rate falls. If the real wage rate is OW2, the demand for labour is more than supply of labour. Hence the wage rate rises. At OW, real wage rate the supply and demand are equal. This is equilibrium.

Assumptions :

- There is no interference of government of the economy.

- Perfect competition in commodity and labour market.

- Full employment.

- Wage flexibility.

- Money does not matter.

- Savings and investment depends on the rate of interest.

- Supply of and demand for labour depends on real wage rate.

Section – B

II. Answer any Eight of the following questions in not exceeding 20 lines each. (8 × 5 = 40)

Question 6.

Explain welfare definition.

Answer:

Alfred Marshall tried to remedy the defects of wealth definition in 1890. He shifted emphasis from production of wealth to distribution of wealth.

According to Marshall “Political economy or Economics is a study of mankind in the ordinary business of life. It examines that part of individual and social action which is most closely connected with the attainment and with the use of material requisites of well-being. Thus Economics is on one side, a study of wealth and on the other and more important side, a part of study of man”.

Edwin Cannan defined it as “The aim of political economy is the explanation of the general causes on which the material welfare of human beings depends”. In the words of Pigou ‘The range of enquiry becomes re-stricted to that part of social welfare that can be brought directly or indirectly into relation with the measuring rod of money”.

The main features of Welfare definition :

1) Economics as a social science is concerned with man’s ordinary business of life.

2) Economics studies only-economic aspects of human life and it has no concern with.the social, political and reli-gious aspects of human life. It examines that part of indi-vidual and social action which is closely connected with acquisition and use of material wealth for promotion of human welfare.

3) According to Marshall, the activities which contribute to material welfare are considered as economic activities.

4) He gave primary importance to man and his welfare and to wealth as means for the promotion of human welfare.

Criticism:

1) Robbins criticised Marshall’s economics is a ‘social sci-ence’ rather than a humanscience, which includes the study of actions of every human being.

2) Marshall’s definition mainly concentrated on the welfare derived from material things only. But non – materialistic goods which are also very important for the well being of the people. Hence, it is incomplete.

3) Critics pointed out that quantitative measurement of wel-fare is not possible. Welfare is a subjective concept and changes according to time, place and persons.

4) According to Marshall, economics deals with those ac-tivities of men which will promote human welfare. But production of alcohol and drugs do not promote human welfare. Hence the scope of economics is limited.

5) Another important criticism is that it is not concerned with the fundamental problem of scarcity of resources. According to Robbins the economic problem arises due to unlimited wants and limited resources. These factors are ignored in this definition.

Question 7.

What are various economic investigations?

Answer:

According to Peterson “The term method refers to the techniques and producers used by economists for both construction and verification economic principles. There are mainly two methods used by the economists for conducting economic investigations. They are :

1) Deductive method

2) Inductive method.

1. Deductive method:

This method is also known as the analytical and abstract method. The method of studying phenom-enon by taking same assumptions and deducing conclusions from those assumptions is known as the deductive method. It proceeds from general to the particular or from universal to the individual. This was advocated by economists belonging to the classical school. There are four steps involved in drawing inference through deductive method.

They are :

- Selecting the problem

- Formulating assumptions

- Formulating hypothesis

- Verifying the hypothesis.

The law of diminishing marginal utility is one law derived using this deductive method.

Merits of deduction:

- It is less expensive and less time consuming.

- It analyses complex economic phenomena and bring exact¬ness to economic generalisations.

- It helps in laying down basic principles of human behaviour. Inspite of the above stated advantages, it is not free from limitations. It is based on unrealistic assumptions with little em-pirical content.

2. Inductive method:

This method is also known as Histori-cal, Empirical, Concrete, Ethical or Realistic. This method was strongly advocated and made use of by economists belonging to the historical school. This method proceeds from a part to the whole from particular to general or from the individual to the universal.

The following are the important steps involved in deriving economic generalisations through inductive method.

- Selection of the problem

- Collection of data

- Observation

- Generalisation

Merits of induction method :

1) It is nearer to reality and therefore expected to depict reality.

2) This method involves less chances of mistakes. Inspite of several advantages it has its own defects. This method is expensive and time consuming. It can be used by those who possess skill and competance in handling complex data.

![]()

Question 8.

Explain the importance of law of equi-marginal utility.

Answer:

The law of equi-marginal utility states that a consumer will be in equilibrium when the marginal utility of the various commodity are equal.

Importance :

- Basis of consumer expenditure: It is basis for consumers expenditure and guide the consumers while allocating resources.

- In the field of production: This law is useful to the pro-ducer and it explains how a producer maximises his prof-its and reduces cost of production.

- Exchange: In all our exchanges, this law works, for exchange is nothing but substitution of one thing for another.

- Public Fina nce: This law helps the government in the allocation of scarce resources and also the government levied taxes on the basis of this principle.

- Price determination: This principle has an important bearing on the determination of value.

9. Explain the concept of cross demand.

Answer:

Cross demand : Cross demand refers to the relationship between any two goods which are either complementary to each other or substitute for each other. It explains the functional relationship between the price of one commodity and quantity demanded of another commodity is called cross demand.

Dx = f(Py)

Where Dx = demand for ‘X’ commodity

Py = Price of y commodity

f = function

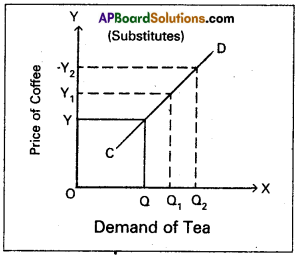

Substitutes: The goods which satisfy the same want are called substitutes. Ex : Tea and coffee; pepsi and coca-cola etc. In the case of substitutes, the demand curve has a positive slope.

In the diagram ‘OX’ axis represents demand of tea and OY axis represents price of coffee. Increase in the price of coffee from OY to OY2 leads to increase in the demand of tea from OQ to OQ2.

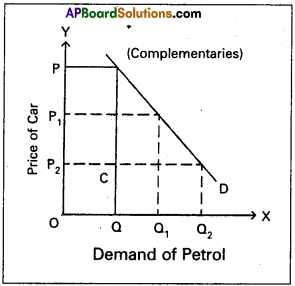

Complementaries:

In case of complementary goods, with the increase in price of one commodity, the quantity demanded of another commodity falls. Ex : Car and Petrol. Hence the demand curve of these goods slopes downward to the right.

In the diagram if price of car decreases from OP to OP2 the quantity demand of petrol increases from OQ to OQ2. So cross demand i.e., CD curve is downward slopes

Question 10.

Explain the point method of measuring price elasticity of demand.

Answer:

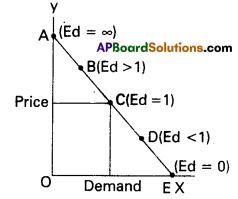

Point method: This method is introduced by Marshall. In this method elasticity of demand is measured at a point on the demand curve. So this method is also called as geometrical method. In this method to measure elasticity at a point on demand curve the following formula is applied.

Ed = \(\frac{The distance from the point to the x – axis}{The distance from the point to the y – axis}\)

In the below diagram, AE is straight line demand curve. Which is 10 cm. length. Applying the formula we get

If the demand curve is non¬linear. It means if the demand curve is not straight line will be drawn at the point on the demand curve where to measure elasticity. In the diagram at C point where Elasticity of demand will be equal to . \(\frac{\mathrm{CB}}{\mathrm{CA}}\)

Question 11.

What are the main features of perfect competition?

Answer:

Perfect competitive market is one in which the number of buyers and sellers is very large, all engaged in buying and selling a homogeneous products without any restrictions.

The following are the features of perfect competition:

1) Large number of buyers and sellers:

Under perfect com-petition the number of buyers and sellers are large. The share of each seller and buyer in total supply or total demand is small. So no buyer and seller cannot influence the price. The price is determine only demand and supply. Thus the firm is price taker.

2) Homogeneous product:

The commodities produced by all the firm of an industry are homogeneous or identical. The cross elasticity of products of sellers is infinite. As a result, single price 11 rule in the industry.

3) Free entry and exit:

In this competition there is a freedom of free entry and exit. If existing firms are getting profits. New firms enter into the market. But when a firm getting losses, it would leave to the market.

4) Perfect mobility of factors of production:

Under perfect competition the factors of production are freely mobile between the firms. This is useful for free entry and exits of firms.

5) Absence of transport cost:

There are no transport cost. Due to this, price of the commodity will be the same throughout the market.

6) Perfect knowledge of the economy:

All the buyers and sellers have full information regarding the prevailing and future prices and availability of the commodity. Information regarding market conditions is availability of commodity.

Question 12.

Explain the concept of scarcity of rent.

Answer:

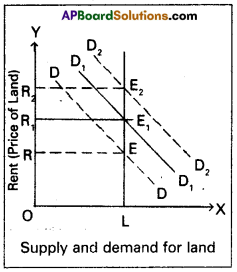

Marshall explained the concept of scarcity of rent on the basis of demand and supply. In general land has indirect demand or derived demand. If there is an explosion of population demand for land increases this result rise in its price. The surplus earned by land above its price is called scarcity rent. The supply of land is fixed and inelastic. The demand for land will determine the rent by influencing its price. Hence rent arises due to the scarcity in the supply of factors of production.

In the side diagram on ‘OX’ axis represent supply and demand for land. ‘OY axis represents Rent.

SL is supply of land. It is perfectly inelastic when ‘DD’ curve shifts upward to D1 D1 So price increases from OR to OR1 Similarly if demand curve further shifts from D1D1 to D2D2 rent price further increases from OR1 to OR2.

Question 13.

What is National income at fadtor cost?

Answer:

The cost of production of good is equal to the rewards paid to the factors which participated in the production process. So the cost of production of a firm is the rent paid to land, wages paid to labour, interest paid on capital and profits of entrepreneur. These are received by suppliers of factors of production. There is a difference between net national income at market prices and national income at factor of cost.

Imposition of tax increases the market prices. When these taxes deducted from net national income, remaining income gets distributed among the factors of production. Sometimes, the government may offer subsidies to encourage production of certain goods. The market prices of such goods will decrease to that extent. The value of subsidies is not included in net national product. So it is to be added.

National income at factor cost = NNP + Subsidies – indirect taxes

![]()

Question 14.

Explain the criticism against the classical theory of employment

Answer:

The classical theory of employment came in for severe criticism from J.K. Keynes. The main points of criticism are as follows :

- The assumption of full employment is unrealistic. It is rare phenomenon and not a normal features.

- The wage cut policy is not a practical policy in modem times. The supply of labour is a function of money wage and not real wage. Trade unions would never accept any reduction in the money wage rate.

- Equilibrium between savings and investment is not brought about by a flexible rate of interest. Infact, savings a function of income and not interest.

- The process of equilibrium between supply and demand is not realistic. Keynes commented the self adjusting mechanism does not always operate.

- Long run approach to theproblem of unemployment is also not realistic. Keynes commented, ‘We are all dead in the long run”. He considered unemployment as a short run problem and offered immediate solution through his employment theory.

- It is not correct to say that money is neutral money acts not only as a medium of exchange but also as a store of value money influences variables like consumption, investment and output.

Question 15.

Write a note on Reserve Bank of India.

Answer:

Reserve Bank of India is the central bank of India. It was established in April 1935, with a share capital of ₹5 crores. It was originally owned by private shareholders and was nationalised by the government of India in 1949. It performs all the functions of central bank according to the “Reserve Bank of India Act 1934”. The main objectives of Reserve Bank of India are :

- Regulating the issue of currency notes.

- Providing guidance to the commercial banks.

- Controlling the credit system of the economy.

- Achieving the monetary stability in the economy.

- Implementing the uniform credit policy throughout the country.

Question 16.

Explain the effects of inflation on distribution.

Answer:

Effects of inflation:

A period of prolonged persistent and continuous inflation affects everyone in the economy it effects production and distribution. Income and employment etc., it is goods so long as it is under control of the economy.The effects of inflation can be discussed under two sub-heads.

1) Effects on production

2) Effects on distribution

Effects on distribution:

Inflation produces a deep impact on the distribution of income’and wealth of society. A prolonged ‘ period of inflation results in the distribution of wealth in favour of inflation on various groups of society are as follows.

1) Debtors and creditors:

During inflation debtors are gen-erally the gainers while the creditors are the losses. The reason is that the debtors had borrowed when the pur-chasing power of money was high and now return the loans when the purchasing power of money is low due to rising prices.

2) On fixed income groups:

Those who get fixed income lose from inflation. Salaried persons people living on past savings, pensioners, interest earners are the worst suf¬fers during inflation because their income remain fixed.

3) On working class:

During inflation working class also suffers worst because wages do not rise as much as the prices of commodities. In addition there is a time lag be-tween the rise in prices and rise in wages. If the trade unions are strong they may get equal increase in money incomes compared to rise in prices.

4) Entrepreneurs:

They experience windfall gains as the prices at their stocks suddenly go up. Inflation thus re-distributes income and wealth in such away as to harm the interest of creditors, labours, fixed income groups and favours the businessmen traders and debtors. By mean¬ing the rich richer and poor poorer, inflation is socially undesirable.

Question 17.

Calculate median from the following data.

Answer:

Section – C

III. Answer any fifteen of the following questions in not exceeding 5 lines each. (15 × 2 = 30)

Question 18.

Marginal utility

Answer:

Marginal utility is the additional utility obtained from the consumption of additional unit of the commodity.

MUn = TUn – TU(n-1)

(Or)

MU = \(\frac{\Delta \mathrm{TU}}{\Delta \mathrm{Q}}\)

Question 19.

Consumer’s equilibrium

Answer:

The term equilibrium implies a position of rest or changelessness. A consumer attains equilibrium only when he secures maximum satisfaction out of his expenditure in distributing a commodity among various uses, the consumer will secure maximum satisfaction if the marginal utility of the commodity equilised in all its uses.

\(\frac{M U_x}{P x}=\frac{M U_y}{P y}\) …. and so on.

Question 20.

Income demand

Answer:

It shows the direct relationship between the income of the consumer and quantity demanded when other factors remains constant. There is direct relationship between income and demand for superior goods inverse relationship between income and demand for inferior goods.

Dx = f(y)

Question 21.

Indifference curve

Answer:

It represents the satisfaction of a consumer from two goods of various combinations. It is drawn on the assumption that for all possible combinations of the two goods on an indiference curve. The satisfaction level remains the same.

Question 22.

Budget line or Price line

Answer:

The budget line or price line shows all possible combinations of two goods that a consumer can buy with the given income of the consumers and prices of the two goods.

Question 23.

Production function

Answer:

The production function is the none for the relation between the physical input and physical output of a firm production of a firm. Production function explains the functional relationship between inputs and outputs this can be follows as Gx = f (L, K, R, N, T)

Question 24.

Supply

Answer:

The quantity of a commodity that a seller is prepared to sell at a particular price and at a particular time is known as supply. Supply curve slopes upwards from left to right it has a positive slope.

![]()

Question 25.

Market

Answer:

Market is place where the commodities are brought and sold and where buyers and sellers meet. Communication facilities help us today to purchase and sell without sell without going to the market. All the activities take place is now called as market.

Question 26.

Monopolistic competitions

Answer:

It is a market where several firms produce same commodity with small differences is called Monopolistic competition. In this market producers to produce close substitute goods. Ex : Soaps, Cosmetics etc.

Question 27.

Marginal revenue

Answer:

Marginal revenue is the additional revenue earned by selling one more unit of the product.

MR = \(\frac{\Delta \mathrm{TR}}{\Delta \mathrm{Q}}\)

Question 28.

Real cost

Answer:

dam Smith regard pair and sacrifices of labour as Real cost. Marshall thought that the efforts and sacrifices under gone by the labourers and capitalists in producing a commodity are the Real costs. So it cannot be measured interms of money.

Question 29.

Full employment

Answer:

Full employment is a situation in which all those who are ‘ willing to work at the existing wage rate are engaged in work.

Question 30.

Liquidity

Answer:

Liquidity means the ease with which one can convert a financial asset into a medium of exchange liquidity is greatest for money as an asset because money itself is a medium of exchange. Infact money is the only asset which possess perfect liquidity.

Question 31.

Net profit

Answer:

Net profit is the economic profit of pure business profit. Net profit is the residue obtained by deduction explicit and implicit cost from the total revenue of a firm.

Question 32.

Primary deposit

Answer:

It is a deposit directly received by commercial banks from the public credit is created from out of the primary deposits of money the customers received from public. A part of the total amount of these deposits given as loans and advances to its customers.

Question 33.

Inflation

Answer:

The term inflation refers to persistent rise in the general price level over a long period of time. Money supply increase money value will be fallen results is purchasing power will be decline.

![]()

Question 34.

Credit money

Answer:

This is also called Bank Money. This is created by commercial banks. This is refers to the bank deposits that are repayable on demand and which can be transferred from one individual to the other through cheques.

Question 35.

What is mode?

Answer:

Mode is most frequently occuring value in data.

Question 36.

Find the mean from the following values X : 43,45, 68, 55, 33, 57, 40, 48, 77, 60

Answer:

Question 37.

What is subdivided Bar Diagram?

Answer:

These diagrams are used to represent various parts of the total.