Students must practice these AP Inter 2nd Year Accountancy Important Questions 5th Lesson Partnership Accounts to boost their exam preparation.

AP Inter 2nd Year Accountancy Important Questions 5th Lesson Partnership Accounts

Very Short Answer Questions

Question 1.

Define partnership.

Answer:

When two or more persons enter into an agreement to carry on business and share its profits / losses is called a “partnership”.

Sec 4 of the Indian Partnership Act 1932 defines partnership as “the relation between persons who have agreed to share the profits of a business carried on by all or any one of them acting for all”.

Question 2.

What are the features of Partnership firm?

Answer:

The essential features of partnership are:

- To form a partnership, there must be at least two persons.

- It is created by an agreement.

- The agreement should be carrying on some legal business.

- The partners should be shared profits and losses of a business.

- No partner can transfer his share to any one without the consent of all other partners.

- All the partners have a right to manage the business with mutual agency.

Question 3.

What is meant by a partnership deed?

Answer:

A document which contains the terms of partnership as agreed among the partners is called “partnership deed”. It contains information about all aspects affecting the relationship among partners.

![]()

Question 4.

Why is it important to have a partnership deed in writing ?

Answer:

After selecting partners it is desirable to draft the partnership deed. As per India Partnership Act 1932 a partnership agreement may be oral or written. But in practice oral agreements can not serve as an evidence in future disputes among the partners. Hence it should be in written, duly stamped and sealed. It can also registered in the court of law. Then the deed enjoys a legal status.

Question 5.

In the absence of partnership deed, what are the rules applicable to partnership firm?

Answer:

When there is no agreement among the partners the following rules will be applicable as per Sec 13 of the Indian Partnership Act 1932.

- Profits or losses of the firm will be shared equally by the partners.

- Interest on capital will not be allowed.

- No interest will be charged on the drawings of the partners.

- If any partner has given some loan to the firm he is entitled to get interest on such amount @ 6% per annum.

- No salary or commission will be allowed to any of the partners.

Question 6.

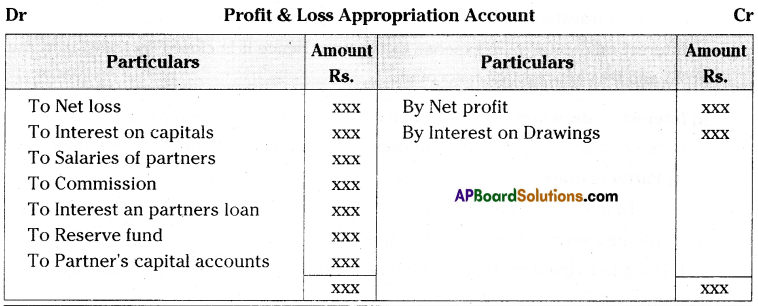

Why is the Profit and Loss Appropriation Account prepared? Explain.

Answer:

After the preparation of Profit and loss account, entries pertaining to partners like interest on capital, drawings, salaries etc., are adjusted against separate account is called “Profit and Loss Appropriation Account”.

It starts with net profit / net loss as per profit and loss account. It is debited with interest on capitals, partner’s salaries, commission etc., and credited with interest on drawings of the partners. The balance of net profit / loss is to be shared among the partners.

Question 7.

What do you understand by fixed capital of partners ?

Answer:

There are two methods of recording partner’s capital accounts

a) Fixed Capital Method b) Floating or Fluctuating Capital Method

a) Fixed Capital Method: Under this method the original capital invested by the partner remains unchanged.

Current accounts are used to record all other transactions i.e., interest on capital, salary commission, a share of profit / loss are credited to current account. It is balanced if it is credit balance shown on the liabilities side and a debit balance on the asset side of the balance sheet.

Question 8.

What do you understand by fluctuating capital of partners ?

Answer:

Under this method capital accounts of the partners fluctuating year to year. All adjustments are made in the partner’s capital accounts.

Interest on capital, salary, commission share of profit are credited in the capital account and drawings, interest on drawings, losses are debited to the capital ac¬counts. The balances are shown in the balance sheet.

Question 9.

How will you deal with the following terms while preparing partnership accounts ?

i) Interest on capital ii) Interest on drawings iii) Interest on Loan

Answer:

i) Interest on capital: Interest is allowed on capital when there is a provision in the deed. When it is allowed.

Interest on capital is an expense to the firm. Hence it is closed by transfer to the profit and loss appropriation account.

Interest on capital is an expense to the firm. Hence it is closed by transfer to the profit and loss appropriation account.

ii) Interest on drawings: It is charged if provided in the partnership deed. It is charged to discourage the partners to withdraw huge amounts from the business, then

It is a gain to the firm. Hence it is to be credited to the Profit & Loss appropriation account.

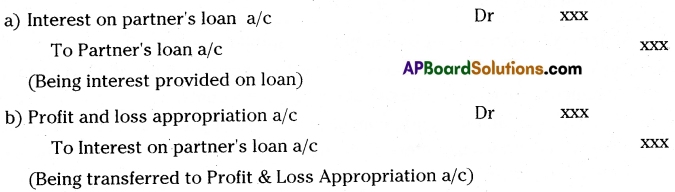

iii) Interest on Loan: Some times a partner may advance a loan to the firm over and above capital contributed. Interest is calculated as per partnership deed. In the absence of deed 6% interest is provided on loan of the partner and charged against profits of the firm.

![]()

Exercise

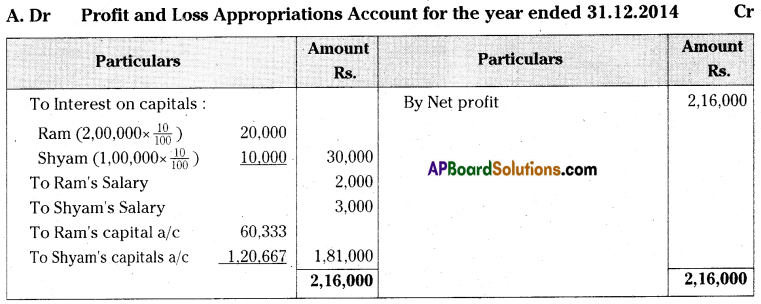

Question 1.

Ram and Shyam started a partnership firm on 1st January, 2014. Their capital contributions were Rs. 2,00,000 and Rs. 1,00,000 respectively. The partnership deed provided:

i) Interest on capitals @10% p.a.

ii) Ram to get a salary of Rs. 2,000 p.a. and Shyam Rs. 3,000 p.a.

iii) Profits are to be shared in the ratio of 1: 2.

The profits for the year ended 31st December, 2014 before making above appro-priations were Rs. 2,16,000. Prepare Profit and Loss appropriation Account.

(Ans: Profit transferred to Ram’s Capital Rs. 60,333 and Shyam’s Capital Rs. 1,20,667) ’

Answer:

Working Notes:

Net profit = 1,81,000;

Ram’s Share 1,81,000 x 1/3 = 60,333;

Shyam’s share 1,81,000 x 1/3 = 1,20,667

Question 2.

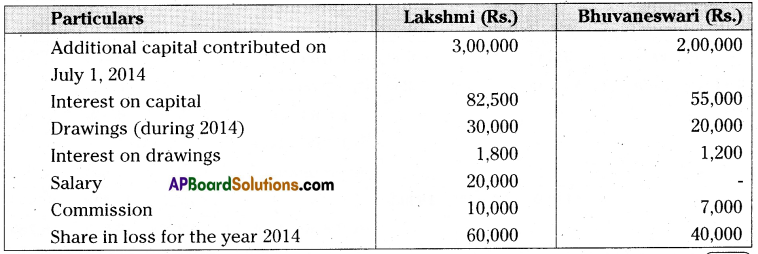

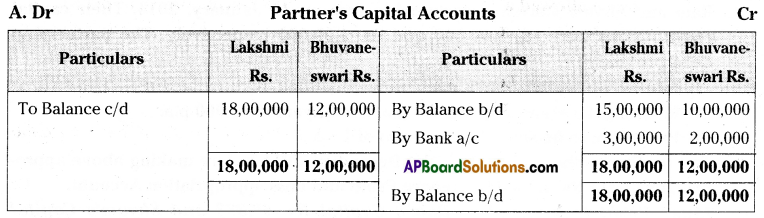

Lakshmi and Bhuvaneswari are partners with capitals of Rs. 15,00,000 and Rs. 10,00,000 respectively. They agree to share profits in the ratio of 3: 2. Show how the following transactions will be recorded in the capital accounts of the partners in case the capitals are fixed. The books are closed on March 31, every year.

(Ans: Capital Accounts of Lakshmi, Rs. 18,00,000 and Bhuvaneswari, Rs. 12,00,000; Current Accounts of Lakshmi, Rs. 20,700 and Bhuvaneswari, Rs. 800)

Answer:

![]()

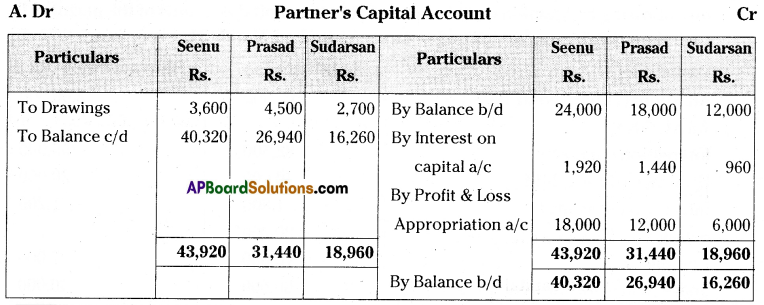

Question 3.

On March 31,2013, after the close of books of accounts, the capital accounts of Seenu, Prasad and Sudarsan showed balance of Rs. 24,000 Rs. 18,000 and Rs. 12,000 respectively. After all adjustments profit for the year ended March 31,2014, amounted to Rs. 36,000 and the partner’s drawings had been Seenu, Rs. 3,600; Prasad, Rs. 4,500 and Sudarsan, Rs. 2,700. The interest on capital @ 8% and the profit sharing ratio of Seenu, Prasad and Sudarsan was 3:2:1. Prepare Partners’ capital Accounts. (Ans: Capi¬tal Accounts of Seenu Rs. 40,320; Prasad, Rs. 26,940; Sudarsan, Rs. 16,260)

Answer:

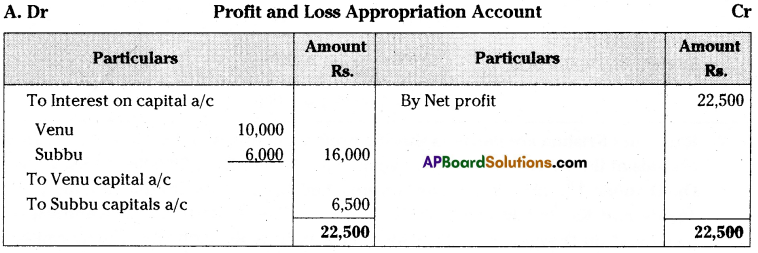

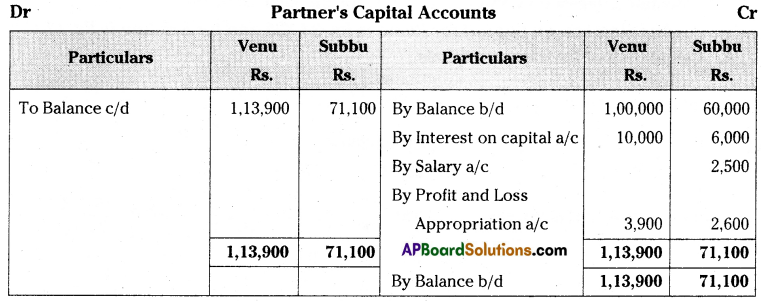

Question 4.

Venu and Subbu are partners sharing profits in the ratio of 3: 2, with capitals of Rs. 1,00,000 and Rs. 60,000 respectively. Interest on capital is agreed @ 10% p.a. Subbu is to be allowed an annual salary of Rs. 2,500. During the year 2014-15, the profits prior to the calculation of interest on capital but after charging Subbu’s salary amounted to Rs. 22,500.

Prepare Profit and Loss Appropriation Account and the partners’ capital ac-counts for the year ending March 31, 2015.

(Ans: Profit transferred to capital A/c Rs. 6,500; Venu’s Capital A/c Rs. 1,13,900 and Subbu’s Capital A/c Rs. 71,100)

Answer:

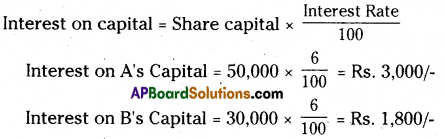

Question 5.

A and B are partners sharing profits in the ratio of 3: 2, with capitals of Rs. 50,000 and Rs. 30,000 respectively. Interest on capital is agreed to be paid @ 6% p.a. calculate interest on capital.

(Ans: Interest on capital of A, Rs. 3,000 and B, Rs. 1,800)

Answer:

Calculation of Interest on capitals:

Question 6.

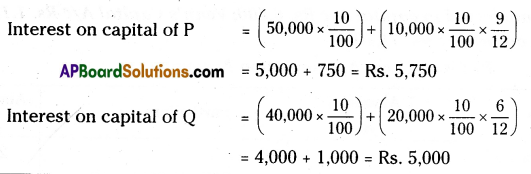

P and Q are partners sharing profits and losses in the ratio of 3: 2. On 1st April 2014 their capital balances were Rs. 50,000 and Rs. 40,000 respectively. On 1st July 2014, P brought Rs. 10,000 as his additional capital, whereas Q brought Rs. 20,000 as additional capital on 1st October 2014. Interest on capital was provided @ 10% p.a. Calculate the interest on capital of P and Q on 31st March 2015.

(Ans: Interest on Capital for P is Rs. 5,750 and for Q is Rs. 5,000)

Answer:

Calculation of Interest on capitals:

![]()

Question 7.

Rama and Krishna are partners sharing profits and losses in the ratio of 5; 1. Their capitals at the end of the financial year 2013-14 were Rs. 1,50,000 and Rs. 75,000. On October 1st, 2014 Rama and Krishna had brought additional capitals of Rs. 16.0 and Rs. 14,000 respectively. On November 1st 2014 Rama withdrew Rs. 6. and on December 1st 2014 Krishna withdrew Rs. 9,000 from their capitals.

Calculate interest on Capital @15% p.a. for the year 2014-15. *

(Ans: Interest on Capital for Rama is Rs. 23,325 and for Krishna is Rs. 11,850)

Answer:

Calculation of Interest on capitals:

= 22,500 + 1,200-375

= Rs. 23,325

= 11,250 + 1,050-450

= 12,300 – 450

= Rs. 11,850

Question 8.

Priya and Mani are partners, sharing profits and losses in the ratio of 5: 3. The balances in their capital accounts as on April 1, 2013 were; Priya, Rs. 6,00,000 and Mani, Rs. 8,00,000. Calculate interest on capital; (a) when there is no agreement in respect of interest on capital, and (b) when there is an agreement that the interest on capital will be allowed @7% p.a.

(Ans: (a) No interest on Capital; (b) for Priya is Rs. 4,200 and for Mani is Rs. 5,600)

Answer:

a) When there is no agreement:

Interest on capital of Priya = No Interest

Interest on capital of Mani = No Interest

b) When there is an agreement that the interest on capital will be allowed 7% p.a..

Interest on capital of Priya = 6,00,000 x 7/100 = Rs. 42,000

Interest on capital of Mani = 8,00,000 x 7/100 = Rs. 56000

Question 9.

Mohith is a partner, who withdrew Rs. 5,500 at the end of June, 2014. The partnership deed provides for charging the interest on drawings @12% p.a. Calcu-late interest on Mohith’s drawings for the year ending 31st December, 2014.

(Ans: Interest on Drawings Rs. 330)

Answer:

Calculation of Interest on drawings:

Question 10.

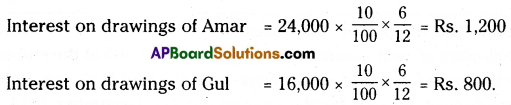

Amar and Gul are partners in a firm. They share profits in the ratio of 3: 2. As per their partnership agreement, interest on drawings is to be charged @10% p.a. Their drawings during 2014 were Rs. 24,000 and Rs, 16,000, respectively. Calculate interest on drawings.

(Ans: Interest on Amar’s Drawings, Rs. 1,200 and Gul’s Rs. 800) (Hint: If the date of Drawings is not given in the question, interest on drawings will be charged and average period of 6 months)

Answer:

Calculation of Interest on drawings:

Note: It date of drawings is not given. Interest is calculated for average period of 6 months.

Question 11.

Bose is a partner is a firm. He withdraws Rs. 3,000 at the starting of each month for 12 months. The books of the firm close on March 31 every year. Calculate interest on drawings if the rate of interest is 10% p.a. (Ans: Interest on Dra wings, Rs. 1,950)

Answer:

Calculation of Interest on drawings of Bose:

When the amount is withdrawn at the beginning of every month:

Total drawings = 3,000 x 12 = Rs. 36,000

Interest on drawings = 36,000 x 10/100 x 6.5/12 = Rs. 1,950.

![]()

Question 12.

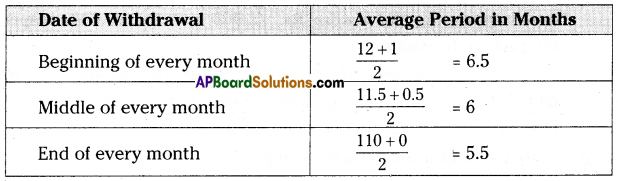

Vishnu and Thomas are partners in a firm. They share profits equally. Vishnu’s monthly drawings are Rs. 2,000. Interest on drawings is to be charged @ 10% p.a. Calculate interest on Vishnu’s drawings for the year 2014, assuming that money is withdrawn: (!) in the beginning of every month, in the middle of every month, and Qii) at the end of every month.

(Ans: Interest on Drawings (?) Rs. 1,300; (a) Rs. 1,200; (???) Rs. 1,100)

Answer:

Calculation of interest on drawings of Vishnu:

i) When the amount is withdrawn at the beginning of every month:

Total drawings = 2,000 x 12 = 24,000

ii) When the amount is withdrawn in the middle of every month.

iii) When the amount is withdrawn at the end of every month:

Table showing Average period

Note 1:

Question 13.

A and B are partners sharing profits and losses in the ratio of 4: 1. A withdraws Rs. 2,500 at the beginning of each month and B withdrew Rs. 1,500 at the end of each month for 12 months period. Interest on drawings was charged @ 8% p.a. Calculate the interest on drawings of A and B for the year ended 31st December 2014.

(Ans: Interest on Drawings for A is Rs. 1,300 and for B is Rs. 660)

Answer:

Calculation of interest on drawings of A and B.

a) When the amount withdrawn at the beginning of each month.

Total drawings = 2,500 x 12 = Rs. 30,000

b) When the amount withdrawn at the end of each month.

Total drawings = 1,500 x 12 = Rs. 18,000

Question 14.

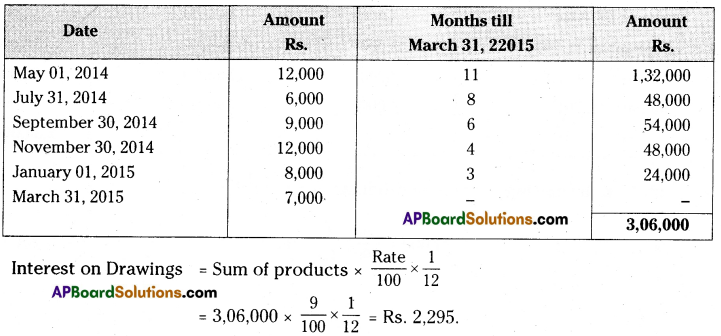

Apama is a partner in a firm. She withdrew the following amounts during the year ended March 31, 2015.

May 01, 2014 – Rs. 12,000

July 31, 2014 – Rs. 6,000

September 30, 2014 – Rs. 9,000

November 30, 2014 – Rs. 12,000

January 01, 2015 – Rs. 8,000

March 31, 2015 – Rs. 7,000

Interest on Drawings charged at 9% p.a. Calculate interest on drawings.

(Ans: Interest on Drawing Rs. 2,295)

Answer:

![]()

Question 15.

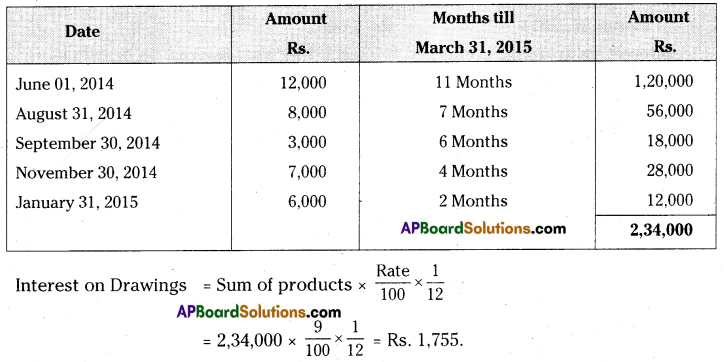

John, a partner in Kaveri Tours and Travels withdrew money for his personal use form his capital account during the year ending March 31, 2015. Calculate interest on drawings in each of the following alternative situations, if rate of interest is 9 per cent per annum.

a) If he withdrew Rs. 3,000 at beginning of each month.

b) If an amount of Rs. 3,000 per month was withdrawn by him at the end of each month.

c) If the amounts withdrawn were:

Rs. 12,000 on June 01, 2014, Rs, 8,000 on August 31, 2014

Rs. 3,000 on September 30, 2014, Rs. 7,000, on November 30, 2014, and

Rs. 6,000 on January 31, 2015.

(Ans: Interest on Drawings (a) Rs. 1,755, (b) Rs. 1,485, and (c) Rs. 1,755)

Answer:

Calculation of interest on drawings of John:

a) When the amount is withdrawn at the beginning of each month:

Total drawings = 3,000 x 12 = 36,000

b) When the amount is withdrawn in the end of each month: Total drawings = 3,000 x 12 = 36,000

c) Amount withdrawn in various dates:

Statement showing Calculation of Interest on Drawings