Students must practice these AP Inter 1st Year Economics Important Questions 4th Lesson Theory of Production to boost their exam preparation.

AP Inter 1st Year Economics Important Questions 4th Lesson Theory of Production

Long Answer Questions

Question 1.

Explain the law of variable proportions. [May, March – 2018, 2017; May 2016]

Answer:

An important law relating to production (producers) is the law of variable proportions. The law states that when a business firm increases one variable factor, keeping the other fixed factors constant, the increase in output is not proportional or not equal to the increase in the quantity of variable input. This law is also known as Law of diminishing returns and was introduced by Prof. Marshall. The law mostly applies in the agricultural sector and is applicable only in the short run.

Definition: Marshall has defined the law as below.

“An increase in the amount of labour and capital applied in the cultivation of land causes, in general, a less than proportionate increase in the amount of output raised, unless it happens to coincide with an improvement in the arts of agriculture”. Assumptions: The law is based on the following assumptions.

- It is possible to change some inputs, keeping other factors/inputs constant to increase production.

- State of technology or methods of production remain constant.

- All units of variable inputs (labour) are homogeneous

- The firm operates in the short period or short run.

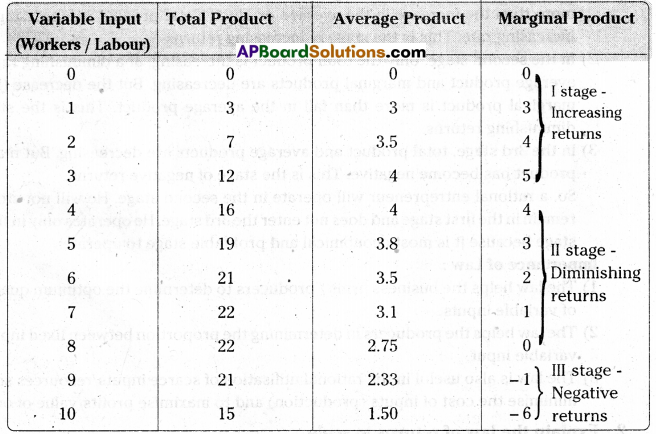

The law can be explained with the help of the following table.

In the above table, when there is an increase in the number of workers, (with the number of machines remaining constant, only one machine) total product (output) is first increasing, remaining constant for sometime and later decreasing. The average product is first increasing and afterwards decreasing. Marginal product is also first increasing later decreasing, becoming zero and finally becoming negative.

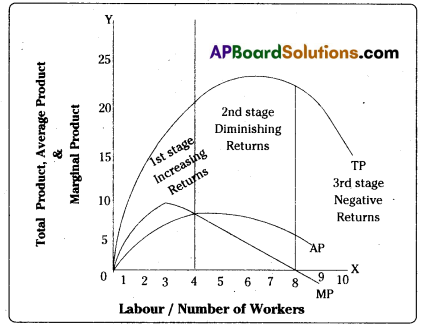

The law can also be explained with the help of the following diagram.

In the above diagram, on Y – axis, Total Product, Average Product and Marginal Product are shown. On X – axis labour or the number of workers is shown.

In the above diagram, there are 3 stages.

1) In the first stage (stage of increasing returns) total product, average product and marginal product are increasing. But the increase in marginal product is greater or more than the increase in the average product. Total product is increasing at an increasing rate. This is the stage of increasing returns.

2) In the second stage, only the total product is increasing, at a diminishing rate, but average product and marginal products are decreasing. But tfce decrease (fall) in marginal product is more than fall in the average product. This is the stage of diminishing returns.

3) In the 3rd stage, total product and average products are decreasing. But marginal product has become negative. This is the stage of negative returns.

So, a rational entrepreneur will operate in the second stage. He will not stop and remain in the first stage and does not enter the 3rd stage. He operates only in the 2nd stage because it is most economical and profitable stage to operate.

Importance of Law:

- The law helps business firms / producers to determine the optimum quantities of variable inputs.

- The law helps the producers in determining the proportion between fixed input and variable input.

- The law is also useful in the rational utilisation of scarce inputs/resources so as to minimise the cost of inputs (production) and to maximise profits/value of output.

Question 2.

Explain the law of returns to scale.

Answer:

The Law of Returns to Scale, which applies in the long run, shows or explains the relationship between inputs and outputs in the long run. In the short run, to make changes in output, it is not possible to the producer to make changes in all the inputs.

He can make changes only in variable inputs, by keeping constant all the fixed inputs.

But in the long run, to increase or make changes in output, the producer can also make changes in fixed inputs.

The law of returns to scale explains, how output changes, in the long run, when there is an increase in the quantities of all inputs, both fixed and variable. When all the inputs are increased, the firm will experience three stages, namely the stage of increasing returns, followed by the stage of constant returns, further followed by the stage of decreasing returns.

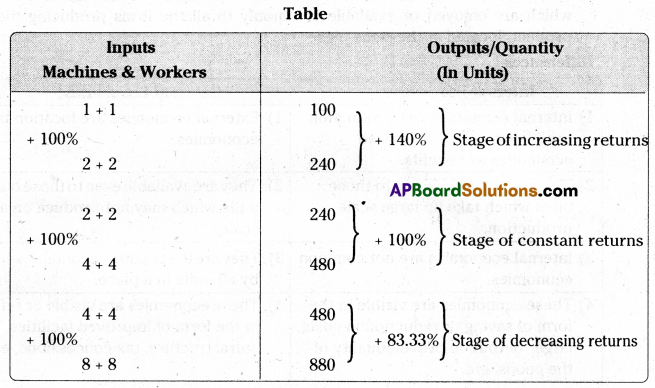

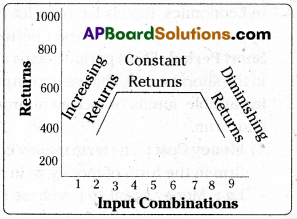

The law of returns to scale can be explained with the help of table and diagram given below.

Stage of Increasing Returns: The producer has increased both the inputs (machines, workers) three times, each time by 100%. When the inputs are increased for the first time, by 100%, the increase in output is 140%. The rate of increase in output is more than proportionate to increase in inputs. So, this is the stage of increasing returns. During the stage of increasing returns, average cost gradually decreases.

Stage of Constant Returns: When the inputs are increased by 100%, 2nd time output has also increased by 100%. The rate of increase in output is exactly proportionate/ equal to the rate of increase in inputs. This is the stage of constant returns. During the stage of constant returns, the average cost also remains constant.

State of Dimishing Returns: When the inputs are increased, 3rd time by 100%, the increase in output is 83.33%. The rate of increase in output is less than proportionate to the rate of increase in inputs. Hence this stage is called stage of diminishing returns. During the stage of diminishing returns, the average cost of the firm gradually increases.

Question 3.

Distinguish between internal economies and external economies.

Answer:

Nowadays, business firms have a tendency to produce goods on a large scale. They do so because when they produce goods on a large scale, they get certain benefits known as economies of scale, also known as economies of large scale production.

Economies of large scale production are of 2 types. They are

- Internal Economies

- External Economies.

1) Internal Economies: Internal economies are those economies or advantages which are available only to those firms which expand their size or take up production on a large scale.

2) External Economies: External economies are those economies or advantages which are enjoyed or available commonly to all the firms producing the same product, located at the same place.

Differences:

| Internal Economies | External Economies |

| 1) Internal economies are production-based or scale or size-based economies or benefits. | 1) External economies are location-based economies. |

| 2) They are available only to those units which take up large-scale production. | 2) They are available even to those business units which may not produce on a large scale. |

| 3) Internal economies are not common economies. | 3) They are the common economies enjoyed by all units in a place. |

| 4) These economies are visible in the form of saving or reduction in costs, larger output, improved quality of the goods, etc. | 4) These economies are visible or reflected in the form of improved facilities, better infrastructure, tax concessions, etc. |

| 5) Internal economies lead to business rivalry, severe competition, and feeling of enmity among business firms. | 5) External economies lead to friendship, co-operation, the spirit of give and take, and sharing among business firms. |

| 6) Internal economies can be compared to the benefit or advantage of textbook reading available to only few textbook reading students in the class. | 6) External economies can be compared to the benefit of expert teaching by a senior teacher, that is enjoyed by all the students assembled in the class. |

Question 4.

Explain short-run cost structure of a Firm.

Answer:

In Economics, time is having a lot of importance. Prof. Marshall has divided time into

- Very short period (Market period)

- Short period

- Long period.

Short Period: Short period means a time period of more than 1 day, but less than 1 year. In the short period, changes in output or quantity can be made only by making changes in variable inputs or factors of production. But fixed inputs cannot be changed in the short run.

1) Money Cost: The term money cost refers to the expenditure or cost incurred by the firm in the form of money or in money terms.

Eg: Money spent to purchase raw materials, wages paid to the workers, etc.

2) Real Cost: According to Prof. Marshall, real costs are not the money costs incurred in the production of a good, but the pains incurred and sacrifices made by labour and capital in the production of goods and services. Real cost is also known as social cost.

3) Opportunity Cost: The opportunity cost of anything is the value of the best alternative that has been foregone/sacrificed. It can be described as the value of next best alternative lost by using the resource/ input in the present use.

Eg: The opportunity cost of using an acre of land for the cultivation of paddy is the value of sugarcane lost (Rs. 40000/-) that could have been raised on that land.

Fixed Costs and Variable Costs:

a) Fixed Cost: Fixed costs are those costs which remain fixed and which do not change with a change in output. They are the costs which the firm has to bear or incur even if there is temporarily shut down or stoppage of production. Fixed costs are also known as overhead costs, indirect costs.

b) Variable Cost: Variable costs are those costs which change in (direct proportion to) directly with a change in output. When there is an increase in output variable costs increase and vice versa. They are known as prime costs. Eg: Raw material costs, cost of fuel, cost of power, etc.

Average Cost: It is the cost incurred on an average (per capita) on each unit produced by the firm. If the average fixed cost and average variable costs are added, we get average cost. Average cost can also be found by dividing the total cost with the output or quantity produced.

AC = AFC + AVC (or)

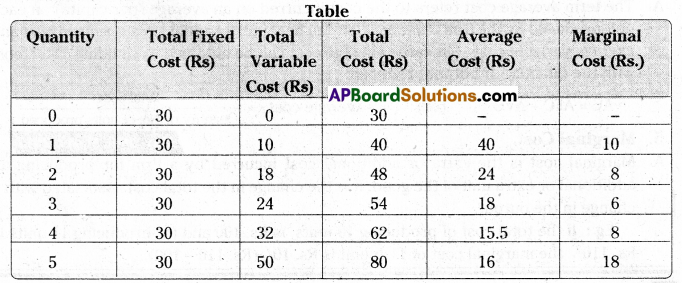

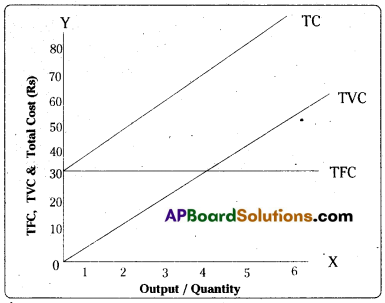

Marginal Cost: It is the additional or extra cost incurred by a firm for producing an extra or additional unit of the good. In other words, it is the change in the total cost associated with a change in output. Eg: If the total cost of 10 units is Rs. 100/- and that of 11 units is Rs. 110/-, the marginal cost of 11th unit is Rs. 10/-. Short run cost structure can be explained with the help of following table and diagram.

In the adjacent diagram, total fixed cost curve is a horizontal straight line parallel to X-axis, because fixed cost is a fixed amount. Total variable cost starts from origin implying that variable cost is nil/ zero, with zero output and varies / increases directly with an increase in output. Total variable cost starts above total fixed cost line implying that total cost is the sum total of total fixed cost and total variable cost.

Question 5.

Explain Internal Economies and External Economies of Scale. [Mar.’19 (AP and TS)]

Answer:

Internal economies are those economies or advantages which are available only to those firms which expand or increase their size and take up production on a large scale.

They are –

1) Technical Economies: They are the advantages which large-sized firms enjoy in the form of use of large-sized machines, use of modern technology, the introduction of division of labour, production of superior quality goods on a large scale, the lower average cost of production, etc.

2) Managerial Economies: They are the advantages which large-sized organisations enjoy in the form of services of specialized managers, better decision-making abilities of talented managers, etc.

3) Marketing Economies: Marketing economies are those advantages which firms operating on a large scale derive in the form of purchase of raw materials at a lower price, lower transportation costs, lower advertisement costs and having the services of marketing experts, etc.

4) Financial Economies: They are the advantages which the large-sized firm operating on large scale enjoy in the form of easy borrowing of the required funds and credit at concessional rates of interest, raising additional capital for the expansion of business, etc.

5) Research and Development: They are the advantages that business units operating on a large scale can have in the form of spending huge amounts on the improvement of technology, improvement in quality of products, the introduction of new products, etc.

6) Risk-bearing Economies: They are the advantages that large firms operating on 1 a large scale enjoy in the form of diversification of products and business, covering losses of some goods through the profits earned from successful products, etc.

External Economies: External economies are those economies or advantages which are available commonly to all firms producing the same or similar units located in the same place. They are

1) Infrastructure Economies: Units producing the same or similar product located in a particular place can enjoy commonly better infrastructure facilities like uninterrupted power supply, availability of skilled labour, improved transport facilities, 24 hours water supply provided by the government.

2) Specialization Economies: The units which are located in large numbers in a given place can easily introduce specialization. Such specialization among the units results in improved performance of every firm. Such specialization among firms also solves the problem of raw material supply and sale of finished goods.

3) Information and Marketing Economies: A large number of firms producing the same or similar goods, located at a given place can have the advantage in the form of the availability of the latest market information relating to the prices of inputs and prices of manufactured goods. Such information can be collected by the information centres collectively established by them.

4) Research Economies: The large number of units producing the same or similar goods established in a particular area can take up collective research activities through the research centres jointly established by them. The findings of the scientists and researchers relating to new products, new technologies, etc. can be used by all the firms.

5) Economies of Welfare: When a number of manufacturing units are located in a particular area, welfare facilities like schools, housing colonies, hospitals, etc. cam be provided by the owners of such units. Such welfare facilities increase the efficiency and productivity of all the workers and all the industrial units are benefited.

Question 6.

Explain the revenue curves in perfect competition.

Answer:

The term revenue generally refers to the amount of money received by a business firm through the sale of the goods produced by it. It is of 3 types.

a) Total Revenue: Total revenue is the sum total amount of money received by a business from the sale of all units of a good. Total revenue can be obtained by multiplying the sale price of the good with the total quantity or output sold.

Total Revenue = Price per unit (AR) x Output or Quantity sold

b) Average Revenue: Average revenue is the revenue obtained on an average (per capita) from each unit sold. It can be obtained by dividing total revenue with the quantity sold or number of units sold.

Total Revenue

![]()

c) Marginal Revenue: Marginal Revenue is the additional or extra revenue received by the firm from the sale of an additional or extra unit of the good.

Marginal Revenue = TRn – TRn-1

Eg: If the total revenue from 2 units is Rs. 20/- and from the sale of 3 units is Rs. 28/-, the marginal revenue of 3rd units is Rs. 8/- (Rs. 28 – 20 = Rs. 8)

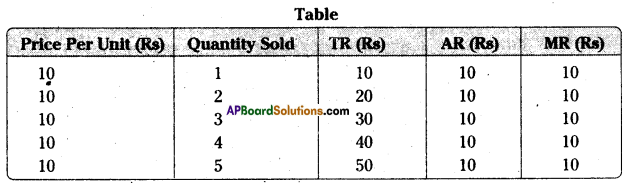

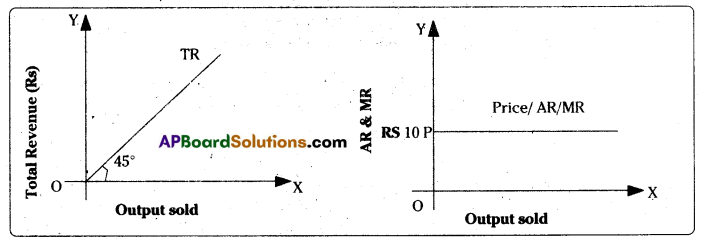

Revenue Curves in Perfect Competition: Under perfect competition, a firm has to sell any quantity at the same price or uniform price. So, the total revenue in perfect competition increases directly (at constant rate) with an increase in the quantity sold. But, Average revenue (price), which is also equal to Marginal revenue will be a horizontal straight parallel to X – axis.

Question 7.

Explain the revenue curves in imperfect competition.

Answer:

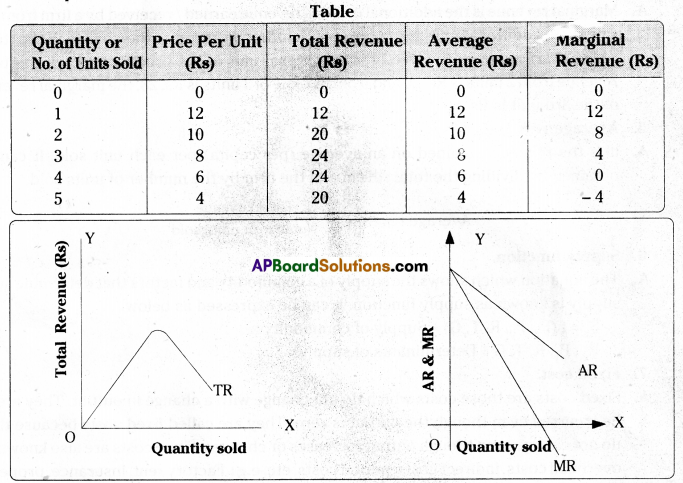

An important form of imperfect competition is Monopoly, where there is a single firm or seller. In imperfect competition/monopoly the firm has to reduce the selling price in order to sell more output. So, when the firm/monopolist sells more units, total revenue increases at a diminishing rate, but the Average Revenue Curve and Marginal Curves decrease and they are downward sloping.

The following table and diagram show the revenue curves (TR, AR, MR) in imperfect competition.

In the above diagram with the sale of additional units, AR is decreasing and MR is also decreasing. MR is below in average revenue curve because the decrease in MR (Rs 4/-) is more than the decrease in Average Revenue (Rs. 2/-). With the sale of additional units, Marginal Revenue becomes zero and also negative later.

Very Short Answer Questions

Question 1.

Production Function.

Answer:

The term production function shows or refers to the technical (or mathematical / functional) relationship between the physical quantities of inputs and physical quantity of output. It,always refers to a period of time and assumes that there is no change in technology.

Q = f (N, L, K, O) where

Q = Quantity of output,

N, L, K, O = Quantities of inputs.

Question 2.

Law of Supply. [May, March 2018; May 2017]

In Economics, the terrific supply refers to the quantities which a seller is prepared to sell at a particular price.

“Other things remaining the same, the supply of a commodity extends (increases) with a rise in the price and contracts (decreases) with a fall in its price.” In other words, the law of supply states that there is a direct and positive, relationship between price and supply.

Question 3.

Factors of Production.

Answer:

In Economics, all those materials, services, individuals, and agents which help in production are known as factors of production. In economics, there are 4 factors of production. They are

- Land,

- Labour,

- Capital,

- Entrepreneur.

Question 4.

Average Cost. [May-2019 (TS)]

Answer:

The term average cost refers to the cost incurred on an average (per capita) on each unit produced by the firm. Average cost can be found by adding average fixed cost and average variable cost. Similarly, average cost can be obtained by dividing total cost with the quantity or output produced.

AC = AFC + AVC (or)

![]()

Question 5.

Marginal Cost. [May 2016, March 2017]

Answer:

Marginal cost is the extra or additional cost incurred by a firm for producing an additional or extra unit of the good. It is the change in the total cost associated with a change in the output.

Eg: If the total cost of producing 10 units is Rs. 100 and for producing 11 units is Rs.. 110/, the marginal cost of 11th unit is Rs. 10/- (Rs. 110 – 100).

Question 6.

Real cost.

Answer:

According to Prof. Marshall, real costs are not the money costs incurred in the production of a good, but the pains and efforts of labour and the efforts and sacrifices made by capitalists in the production of a good and service. It is also known as social cost.

Question 7.

Opportunity cost.

Answer:

The opportunity cost of anything is the value of the alternative that has been foregone (sacrificed). It can be described as the value of next best alternative lost as a result of using the resource or input in the present use. e.g: The opportunity cost of using lacre of land for cultivating paddy is the value of sugarcane (Rs. 4,000) that could have been raised on that land.

Question 8.

Total cost.

Answer:

The sum of total of all expenses incurred by a firm for the production of a given quantity of goods in known as total cost. It consists of two parts namely, total fixed cost and total variable cost. In other words, total cost-is the total of total fixed cost and total variable cost. Total cost = Total fixed cost + Total variable cost.

Question 9.

Marginal revenue.

Answer:

Marginal revenue is the additional or extra revenue earned/received by a firm from the sale oi an additional unit of the product. In other words, it is the change in the total revenue arising from the sale of an additional unit of the product, e.g: If the total revenue from 2 units is Rs. 20 and from the sale of 3 units is Rs. 28, the marginal revenue of the 3rd unit is Rs. 8.

Question 10.

Average revenue.

Answer:

It is the revenue obtained, on an average (per capita) per unit sold. It can be obtained by dividing the total revenue of the firm by the number of units sold.

Question 11.

Supply function.

Answer:

The equation which shows the supply of a commodity and factors that determine such supply is known as supply function. It can be expressed as below.

Sx = f (Px, Py, R, T, G) = Supply of commodity x.

Px, Py, R, T, G = Determinants of supply.

Question 12.

Fixed cost.

Answer:

Fixed costs are those costs which do not change with a change in output. They are to be incurred even though the output is zero. They are called fixed costs because they do not change even though output increases or changes. Fixed costs are also known as overhead costs, indirect costs, period costs, etc. e.g: Factory rent, insurance, property taxes.

Question 13.

Variable cost.

Answer:

Variable cost, are those costs which change directly with a change in output. In other words, when there is an increase in output, total variable cost also increases. These costs are also known as prime costs, special costs or direct costs. When there is no production, total variable cost will be zero. They are called variable costs because, they vary or change with a change in output, e.g: Raw material cost, fuel, power, transport, wages of daily workers, etc.

Question 14.

Money costs.

Answer:

The costs incurred in terms of money for producing a good or service are known as money costs, e.g.: Cost of raw materials, wages, rent, salary, other expenses paid in the form of rupees.